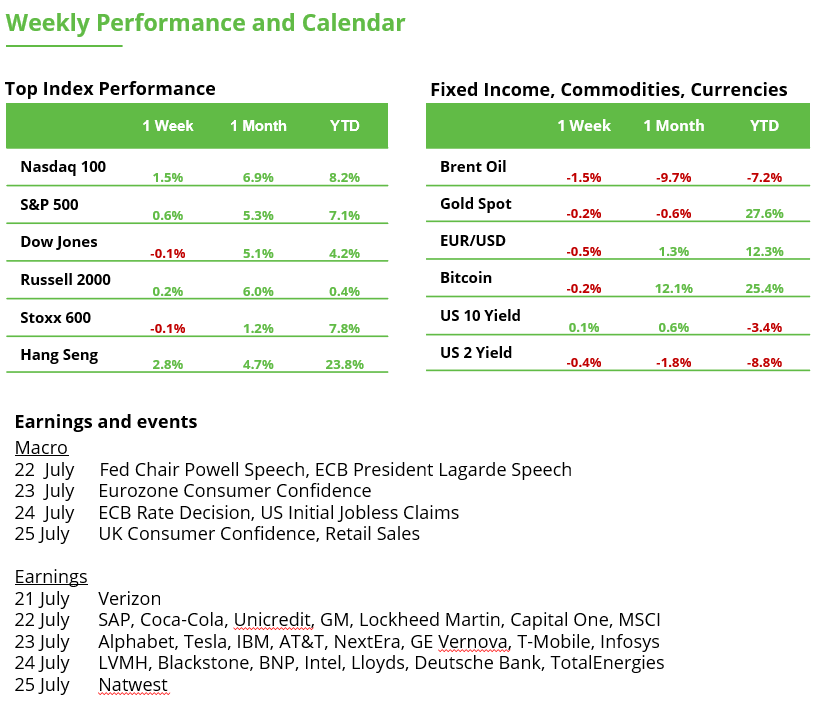

Analyst Weekly, July 21, 2025

Banks Earnings: From Protection to Deployment

We’ve got reviewed earnings calls from main US banks, together with Goldman Sachs, JPM, Blackrock, Citi, Wells Fargo, BNY, BoA, MS, and PNC. The temper has notably shifted, and for the higher.

To us, Banks more and more appear like levered performs on financial normalization and tech infrastructure, not simply rates of interest.

Listed here are our broad takeaways:

Deregulation:

Compliance prices can be a key metric to look at over the approaching months, as they could supply the clearest sign that deregulation is beginning to take maintain. Whereas regulatory modifications usually take time to materialize, declining compliance spend may recommend the early influence of coverage shifts, doubtlessly offering a tailwind to earnings. We anticipate these modifications to help the monetary sector over the following 12 months. Diminished regulatory friction may additionally assist unlock capital markets exercise, together with a pickup in IPOs and M&A.

Earnings transcripts from main banks reinforce this view, exhibiting early indicators that regulatory rollbacks are starting to take impact. Compliance prices, lengthy a drag on profitability, seem like peaking, with some companies guiding for a decline beginning in 2026. On the similar time, reductions in stress capital buffers (SCBs) and anticipated recalibrations of the SLR and GSIB surcharges are growing capital flexibility. Executives broadly welcomed this shift, citing improved situations for capital deployment, deal-making, and competitiveness.

Macro to Micro:

There’s a clear pivot from macro defensiveness to client-driven progress. The strongest momentum is in funding banking, structured credit score, and different methods.

CEO Tone: Sharply Extra Constructive

Executives are decisively extra forward-leaning than in current quarters. Sentiment is particularly robust for companies tied to capital markets, options, and financing.

“The accelerated innovation and disruption from AI is ready to create vital demand-related infrastructure and financing wants.” — Goldman Sachs CEO

“Buyer conduct additionally modified and matched digitization… Now we now have an opportunity to seize the worth of that with the brand new enhanced capabilities of AI.” — Financial institution of America CEO

Strategic Themes Gaining Traction:

AI and Platform Fashions are transferring from testing to monetization.

Capital aid (SCB, SLR, GSIB revisions) is already influencing buyback plans and ROE steering.

IB pipelines are rebounding, with sequential progress in M&A and IPO exercise.

Mortgage progress is modest however enhancing, with indicators of re-leveraging in Prime, ABS, and center market.

AI adoption is actual and firm-wide, banks anticipate measurable margin carry in 2–3 years.

Tokenization goes institutional: main gamers are positioning to anchor digital asset infrastructure.

Dangers: Nonetheless Current, However Downplayed:

Industrial actual property (CRE) and broader credit score issues stay, however administration commentary has shifted from “watchful” to “beneath management.”

Funding Takeaway: Within the US, we predict that banks are benefiting from deregulation, tax certainty, and a situation that will see stabilising inflation with no imminent recession (a steeper curve). After 18+ months of macro warning, banks are shifting into deployment mode, with clearer visibility on regulatory aid, rising consumer demand, and monetization of AI and digital infrastructure investments. From a positioning perspective, we don’t see large-cap banks as simply rate of interest performs; they’re now levered autos on capital markets normalization, personal credit score enlargement, and enterprise tech adoption.

Sector Focus: Broader Financials

IPOs, Credit score, and M&A Choosing Up:

Capital markets exercise is rebounding decisively:

IPO issuance in H1 25 is up ~11% y/y, and greater than +100% versus the lows of 2022 to 2023.

Company bond issuance (IG & HY) stays robust, regardless of powerful comps from 2024.

M&A deal circulate is regular, although deal closures stay a watchpoint.

General, expectations that had overshot post-election and undershot at mid-cycle lows now seem appropriately aligned with precise market exercise. This normalization strengthens the case for sustained upside in financials by year-end.

Fundamentals & Valuations:

Following early Q2 earnings stories, anticipated earnings progress for the sector jumped from 2.7% to 7.8%, whereas income forecasts rose from 1.2% to 2.1%. With deregulation unfolding and a doubtlessly steeper yield curve, profitability may proceed to shock to the upside. Valuations (P/B) have normalized, whereas ROEs stay stable, supporting the funding case.

Deregulation Tailwinds:

The deregulation story stays an essential tailwind for financials over the following 12 to 24 months. Past enhancing profitability, it considerably improves capital flexibility, fueling share buybacks and dividends. Financials have been the second-largest patrons of their very own inventory, repurchasing over $190B up to now 12 months, and that quantity might rise as regulatory constraints ease.

Some of the impactful developments was the slashing of funding for the Shopper Monetary Safety Bureau (CFPB) beneath the brand new tax invoice.The CFPB is the US company answerable for regulating shopper finance merchandise like bank cards, auto loans, and private lending. Slicing its funding is predicted to scale back regulatory oversight and enforcement, significantly for shopper finance companies, that are already exhibiting the strongest upward earnings revisions for 2025 and 2026.

Magazine 7 Earnings Begin This Week

What we’re watching: whether or not firms, particularly the massive tech “hyperscalers” like Amazon, Microsoft, and Google, will maintain spending closely on AI infrastructure. This spending is an element of a bigger capital expenditure cycle that’s been fueling the AI increase.

To date, these firms are prone to keep and even enhance funding, particularly as early indicators present that AI is beginning to increase income.

A key coverage angle comes from the brand new tax invoice within the US, which incorporates enterprise tax incentives geared toward encouraging firms to deliver ahead (pull ahead) their spending into 2025, serving to to offset the price of new tariffs.

Traditionally, tax breaks like full expensing (the place firms can instantly deduct the price of investments) have helped industrial firms, and we predict it may additionally profit software program companies this time, particularly these constructing or promoting AI instruments.

Tesla & Alphabet (July 23): Concentrate on automobile supply developments and cloud progress.

Meta (July 30): Search for particulars on AI/knowledge middle investments and person advert income.

Apple & Amazon (July 31): iPhone demand and AWS profitability + steering.

Nvidia (Aug 27): Investor consideration on Blackwell chip rollout and export restrictions.

Microsoft (July 30): Azure/AI income momentum and margin developments.

GENIUS Act: The US Goes All-In on Stablecoins

The US has signed the GENIUS Act into regulation, the primary main piece of US crypto laws, setting a transparent regulatory framework for the issuance and buying and selling of stablecoins.

This long-awaited readability opens the door for banks, asset managers, retailers, and cost processors to actively enter the stablecoin house with out regulatory ambiguity.

The regulation comes at a pivotal second: stablecoins have turn into the core liquidity layer connecting crypto and conventional finance, enabling quick, dollar-denominated transactions with out friction.

Analysts ought to watch three potential implications:

Capital flows into regulated stablecoin infrastructure might speed up, doubtlessly unlocking trillions in on-chain cost rails, tokenized securities, and automatic finance.

The Act reinforces Ethereum’s dominant place because the core blockchain for stablecoin issuance, on account of its transparency, composability, and institutional adoption.

The subsequent battleground is regulatory readability on the broader crypto market construction: tokenized securities, personal fairness, and custody guidelines are actually in focus.

The GENIUS Act just isn’t the tip of the street—it’s the start of regulated crypto infrastructure at scale on the earth’s largest financial system.

Merchants Eagerly Await The ECB Curiosity Charge Resolution

The ECB will announce its rate of interest choice on Thursday. No change is predicted. Nonetheless, the following press convention with Christine Lagarde may set off volatility within the markets. Traders are hoping for clues concerning the future rate of interest path. Feedback on commerce coverage, inflation dangers and progress prospects will assist assess how the central financial institution views the present scenario, and whether or not the euro’s appreciation in current months is justified.

EURUSD has skilled a decline because the begin of July. In the course of final week, the pair reached the truthful worth hole zone between 1.1543 and 1.1574. Nonetheless, value motion has since entered a sideways vary, as patrons had been held again by one other zone round 1.1650. The broader uptrend stays intact, making a transfer towards 1.18 the most certainly situation. A break under 1.1543, nonetheless, may open the door for sellers to focus on earlier lows at 1.1449 and 1.1373.

EURUSD within the every day chart, correction throughout the uptrend

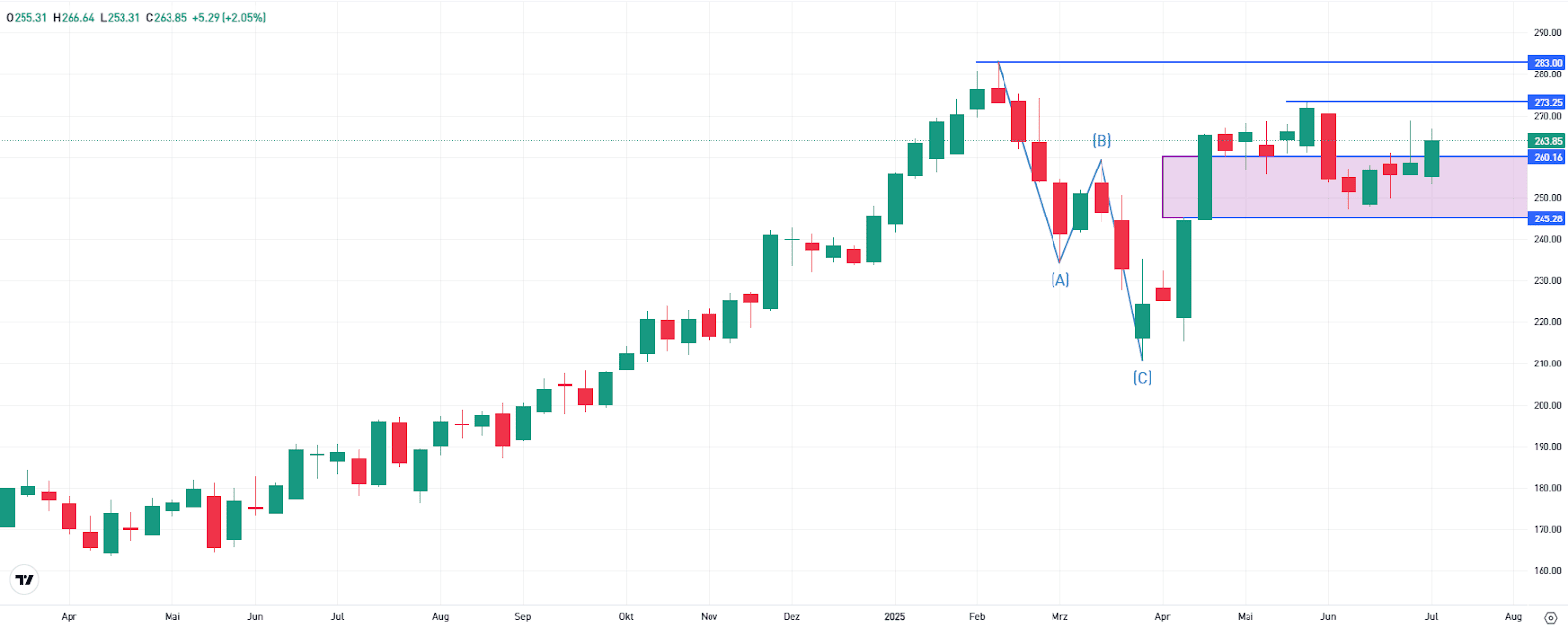

Can SAP Justify the Advance of Belief? Quarterly Outcomes on Tuesday

The SAP inventory, with its value enhance final week, has offered a superb setup to succeed in a brand new file excessive within the coming weeks; it’s 7% away. Nonetheless, the inventory’s excessive valuation makes it weak to short-term profit-taking. The ahead P/E ratio stands at 42, considerably larger than that of friends like Microsoft, Oracle, and Salesforce.

Then again, SAP has constantly demonstrated robust operational efficiency. As well as, the forecasts for the second-quarter outcomes are promising, and analysts see potential for an upward revision of the earnings outlook. In occasions of commerce conflicts, SAP additionally advantages from a structural benefit in comparison with different sectors. The corporate doesn’t promote {hardware} however as an alternative focuses on cloud options and synthetic intelligence, making it solely not directly uncovered to the influence of tariffs.

Technical launchpad?

SAP shares ended final week up 2% at €263. After stabilizing in current weeks, the inventory noticed renewed curiosity inside a medium-term help zone. Following a robust rebound from the April low, a so-called Truthful Worth Hole fashioned – a value hole between €245 and €260. The share value fell again into this zone, the place the sell-off was halted.

Earlier than the April low, the inventory confirmed a textbook ABC correction sample. The present hole to the file excessive is about 7%. For the possibilities of retesting that top to enhance, patrons must push by the June excessive at €273 first.

This communication is for data and training functions solely and shouldn’t be taken as funding recommendation, a private advice, or a suggestion of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out taking into consideration any explicit recipient’s funding aims or monetary scenario and has not been ready in accordance with the authorized and regulatory necessities to advertise unbiased analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product aren’t, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.